Futures and Forwards Flashcards

(58 cards)

NDFs

Nondeliverable forwards

Total return index

Dividends are reinvested into the underlying index

Eurodollar

- US dollar deposits held outside the USA. Based on the LIBOR

- The long position locks in a fixed rate

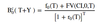

FRA payoff

FRA quotation

A * B

- Contract expires in A months

- At expiration the tenor is (B - A)

- Total duration is B

- FRA price

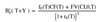

- FRA valuation

- Amount to pay in order to enter the FRA

- Amount to pay or receive in order to exit once held

Forward value at initiation - formula

Forward value at time t - formula

Off-market FRA

The initial value isn’t necessarily set at 0

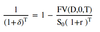

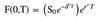

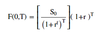

F(0, T) for an underlying paying dividends

PV(D, 0, T) = present value of dividends (actualized from the ex-dividend dates or the actual dividend payment date)

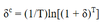

Continuously compounded risk-free rate

Discrete to continuous

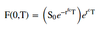

Price of a forward paying a constant dividend at rate deltac

S0 is discounted at the dividend yield rate and equals the present value of the stock without the dividends

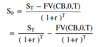

F(0, T) on a coupon-paying bond

- PV(CI, 0, T) = present value of the coupons

- T = time to expiration

- Y = remaining time to maturity at expiration

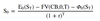

Vt (0, T) for a coupon-paying bond

- The contract expires in T days

- After expiration, the bond has a tenor of Y days

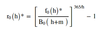

FRA notation

- g - an arbitrary day prior to expiration

- h - the expiration day

- h + m - time until the maturity of the Eurodollar instrument on which the FRA is based

- Li (j) - the rate on a j-day LIBOR deposit on day i

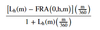

FRA payoff using notation

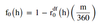

FRA (0, h, m) in function of the Libor rate - formula

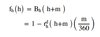

FRA - Vg (0, h, m) formula

F (0, T) - Interest rate parity

F (0, T) for a continuously compounded currency forward

Vt (0, T) for a currency forward

Vt (0, T) for a continuously compounded currency forward at time t

Variation margin

The margin that must be deposited to get back to the inital margin requirement