Fixed Income Flashcards

(105 cards)

Explain the credit valuation adjustment (CVA).

Explain the swap rate curve.

Describe the parameters that define a given CDS product.

Describe convexity.

Explain reduced form models, including assumptions, strengths, and weaknesses.

Explain a positive upfront payment.

Describe the process of calibrating a binomial interest rate tree to match a specific term structure.

Describe credit-default swap (CDS).

Describe ratchet bonds.

Calculate the value of a callable or putable bond from an interest rate tree.

Describe the relationship between forward and spot rates and the shape of the yield curve.

Explain the unbiased expectations theory.

Describe credit events.

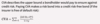

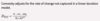

Describe the assumptions concerning the evolution of spot rates in relation to forward rates implicit in active bond portfolio management.

A bond PM would consider the market price of a bond to be less than its value (undervalued) if expected future spot rates are less than quoted forward rates. That is, the market discounts the bonds cash flows by the higher forward rates rather than the lower expected spot rates.

Explain how changes in the level and shape of the yield curve affect the value of a callable or putable bond.

Describe the downside risk of a convertible bond.

Calculate effective duration of a callable or putable bond.

Explain a succession event.

Explain the maturity structure of yield volatilities and their effect on price volatility.

List types of callable bonds.

An American-style callable bond can be called by the issuer at any time, starting with the first call date until maturity.

A European-style callable bond can only be called by the issuer at a single date at the end of the lockout period.

A Bermudan-style callable bond can be called by the issuer on specified dates following the lockout period.

Describe the local expectations theory.

Distinguish between a physical settlement and a cash settlement.

Describe the option analogy in structural models.

Equity holders have an implied option to either pay off liabilities K at maturity by selling assets and receive AT – K or default on the issue and allow debt holders to assume ownership of assets. The choice depends on whether AT – K is positive (liquidate) or negative (default).

Describe the relationship between expected and realized returns on bonds.