•••••••Performance Evaluation•••••••

A portfolio return can be broken up into three components

Portfolio = Market + Style + Active management decisions

A = P - Benchmark

Style Return = Benchmark - Market (in a broad market index, the benchmark is equal to the market and style return = 0)

Pure index strategy = Rf + Rasset category (any benchmark return shall be attributed to style)

•••••••Performance Evaluation•••••••

Properties of a Valid Benchmark

SAMURAI

- Specified in advance – known before being measured

- Appropriate – consistent with managers style and expertise

- Measurable – calculate in a frequent basis

- Unambiguous – known participants and weights

- Reflective of current investment opinions

- Accountable

- Investable – can be purchased

•••••••Performance Evaluation•••••••

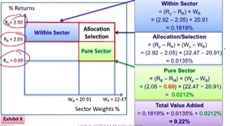

Performance Attribution - Micro Performance Attribution

RV = value-added return (impact on performance)

(+) ∑ (wP − wB) * (RB – RM) pure sector allocation – o/u sector weighting decisions

(+) ∑ (wP − wB) * (RP − RB) allocation/selection interaction – Combination

(+) ∑ wB * (RP − RB) within-sector selection – o/u impact on security selection

Overall benchmark return (RM), Sector Benchmark return (RB), Sector Portfolio Return (RP)

•••••••Performance Evaluation•••••••

Performance Appraisal - Risk-Adjusted Performance Measures

Risk-Adjusted Performance Measures

Ex post alpha uses the security market line (SML) to appraise performance (α>0 above SML). αp = Rp − [RF + βp(Rm − RF)]

Treynor measure = TP = (RP − RF) / βP Appropriate for portfolio where nonsystematic risk has been diversified and β is most relevant

Sharpe ratio = SP = (RP − RF) / σP Appropriate for an undiversified portfolio, where total risk is more relevant

M² = RF + Sharpe Ratio * σM

•••••••Performance Evaluation•••••••

Manager Continuation Policies Guidelines (H0 / HA)

H0: The manager adds no value | HA: The manager adds positive value

Type I error − Rejecting the null hypothesis when it is true. (Keeping managers who are not adding value.)

o Higher significance means more Type 1 error (from 5% to 15%)

Type II error − Failing to reject the null when it is false. (Firing good managers who are adding value.)

o Smaller significance means more Type 2 error (from 15% to 5%)

•••••••Performance Evaluation•••••••

Time Weighted Return vs Money Weighted Return

TWR unaffected by cash-flow (contribution & withdraw)

- Best when manager does not control timing and size of cash flow

- Harder to calculate

- Geometric chain link sub-periods

- (END - CFEND - BEG ) / BEG | (END - BEG + CFBEG) / BEG + CFBEG

MWR = IRR = average rate to each position exposure

- Best when manager controls cash flow

- Higher when there is a large contribution right before the asset goes up or withdraw before it going down

•••••••Performance Evaluation•••••••

Incremental return contribution

Incremental return contribution =

[total fund incremental value contribution - net contributions] / MVbeg

-

Ethical and Professional Standards22

-

Behaviour Finance33

-

Private Wealth Mgt (1)19

-

Private Wealth Mgt (2)12

-

Institutional Investor Portfolios21

-

Economic Analysis18

-

Asset Allocation22

-

Fixed Income18

-

Equity Portfolio Management12

-

Alternative Investment10

-

Risk Management17

-

Trading6

-

Performance Evaluation7

-

GIPS8