P Distributions: Discrete and Continuous (3)

- Probability distribution: gives the probabilities of all possible outcomes of a random variable.

- Discrete distribution: has a finite number of possible outcomes

- Continuous distribution: has a finite number of possible outcomes

P Distributions: Probability Functions

- Discrete random variable: the numbers of days it will rain next week than can take on values : {0,1,2,3,4,5,6,7}

- Continuous random variable: the amount of rain that will fall tonight

- Probability function: p(x) gives the probability that a discrete random variable will take on the value x

P Distributions: Cumulative Distribution Function

A cumulative distribution function cdf, F(x), gives the probability that a random variable will be less than or equal to a given value. For the probability function:

- p(x) = x/ 15 for X = {1,2,3,4,5}

- F(3) = 1/15 + 2/15 + 3/15 = 6/15 = 40%

P Distributions: CDF for a Continuous Distribution

(1) Example: The %ROE, x,for a firm is defined over (-29,+30) and has a Cdf of F(x) = (x + 20) /59. What is the probability that the ROE will be positive and less than or equal to 15? Prob (0

P Distributions: Discrete Uniform

(1) A discrete uniform distribution has a finite number of possible outcomes, all of which are equally likely. For example, p(x) = .2 for X = {1,2,3,4,5} p(2) = 20% F(3) = 69% Prob(2

P Distributions: Binomial Random Variable (2)

(1) The probability of exactly x successes in n trials, given just two possible outcomes (success and failure)

(2) Probability of success on each trial (p) is constant, and all trials are independent

P Distributions: Binomial - Example

What is probability of drawing exactly two white marbles from a bowl of black and white marbles in six tries if the probability of selecting white is .4 each time?

P Distributions: Tracking Error (2)

(1) Tracking error = total return on portfolio - total return on benchmark portfolio or index

(2) Example:

- US Stock portfolio total return = 4%

- S&P 500 total return = 7%

- Tracking error = -3%

P Distributions: Continuous Uniform Distribution

(1) Probability distributed evenly over an interval.

(2) Example: random variable is continuous uniform over the interval 2 to 10.

P Distributions: Properties of Normal Distribution (6)

- Completely described by mean and variance

- Symmetric around the mean (skewness = 0)

- Kurtosis (a measure of peakedness) = 3

- Linear combination of normally distributed random variables is also normally distributed

- Probabilities decrease further from the mean, but the tails go on forever.

- Multivariate normal: more than one random variable, need means, variance and correlation coefficient.

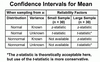

P Distributions: Confidence Interval: Normal Distribution (@)

(1) Confidence Interval: A range of values around an expected outcome. A random variable is expected to be within this range a certain percentage of the time.

(2) Example: the mean annual return (normally distributed) on a portfolio over many years is 11%, and the standard deviation of returns is 8%. Calculate a 95% confidence interval on next years return. —90% conf. int = Xbar+- 1.65s —95% conf. int = Xbar+- 1.96s —99% conf. int - Xbar +- 2.58s 11% +- (1.96((8%)=-4.7% to 26.7%

P Distributions: Standard Normal Distribution

(1) A normal distribution that has been standardized has a mean of 0 and a standard deviation of 1. (2) To standardize a random variable, calculate the z-value. (3) Subtract the mean and divide by the standard deviation. z=X-mean/sd

P Distributions: Calculating Probabilities Using the Standard Normal Distribution

Example: The EPS for a large group of firms are normally distributed an d have a u=$4.00 and a o=$1.50. Find the probability that a selected firm’s earnings are less than $3.70. z= 3.70-4.00/1.50-/20 3.60 is .2 sd below 4.00 mean. Check z table at .2 and .00. For negative z-table, calculate 10 - table value. There is a 42.07% probability that the EPS of a randomly selected form will be more than .20 sd below the mean Iess than $3.70.

P Distributions: Shortfall risk and Roy’s Safety-First Ratio

(1) Shortfall risk: Probability that a portfolio return or value will be below a target return or value. (2) Rou’s Safety-First Ratio: Number of std. dev target is below expected expected return/value. (3) Example: Given the two portfolios, which has the lower probability of generating a return below 5%? —15-5)/12=/93 —18-4/25=.25

P Distributions: Lognormal Distribution

(1) If x is normal, then e^x is lognormal. (2) Lognormal is always positive, used for modeling price relatives –> (1 +return= e^x

P Distributions: Continuous Compounding

(1) Continuously compounding rate = ln(1 + HPR) (2) EAY with continuous compounding = e^i-1 (3) Example: 1-year holding period return = 8% —Continuous compounded rate of return = ln (1.08) = 7.7% —7.7% rate with continuous compounding, EAY = e^.077-1 = 8%

P Distributions: Monte Carlo Simulation (5)

Simulation can be used to estimate a distribution of derivatives prices of NPVs (1) Specify distributions of random variables such as interest rates, underlying stock prices (2) Use computer random generation of variables (3) Value the derivative using those values (4) Repeat steps 2 and 3 1000s of times (5) Calculate mean/variance of all values.

Sampling and Estimation: Sampling (4)

(1) To make inferences about parameters of a population we will use a sample (2) A simple random sample is one where every population member has an equal chance of being selected (3) A sampling distribution is the distribution of sample statistics for repeated sample size n. (4) Sampling error is the difference between a sample statistic and true population parameter.

P Distributions: Historical Simulation (3)

(1) Similar to Monte Carlo simulation, but generates random variables from distributions of historical data. (2) Advantage: Don’t have to estimate distribution of risk factors (3) Disadvantage: Future outcomes for risk factors may be outside the historical range.

Sampling and Estimation: Stratified Random Sampling (2)

(1) Create subgroups from population based on important characteristics (e.g. identify bonds according to callable, ratings, maturity, and coupon. (2) Selected samples from each subgroup in proportion to the size of the subgroup. —Used to construct bond portfolios to match a bond index or to construct a sample that has certain characteristics in common with the underlying population.

Sampling and Estimation: Time-Series vs. Cross-Sectional Data (2)

(1) Time-series data: for example, monthly prices for IBM stocks for five years. (2)Cross-sectional data: for example, returns on all health care stocks last month

Sampling and Estimation: Central Limit Theorem (2)

(1) For any population with mean u and variance o^2, as the size of the random sample gets large, the distribution of sample means approaches normal distribution with a mean u and a varianve o2/n (2) Allows us to make inferences about and construct confidence intervals for population means based on sample means.

Sampling and Estimation: Standard Error of the Sample Mean

(1) standard error of sample mean is the standard deviation of the distribution of sample means. (2) When population is known ox=o/sq.rt n When population is unknown sx =s/sq.rt n

Sampling and Estimation: Standard Error of the Sample Mean-Example

(1) Example: The mean P/E for a sample of 41 firms is 19.0, and the standard deviation of the population is 6.6. What is the standard error of the sample mean? ox=o/sq.rt n = 6.6/sq.rt 41 = 1.03 (2) Interpretation: for sample size n=41, the distribution of the sample means would have a mean of 19.0 and a standard deviation of 1.03.

-

Ethical and Professional Standards96

-

Quantitative Methods: Basic Concepts66

-

Quantitative Methods: Applications77

-

Wrong Answers60

-

Economics: Microeconomic Analysis109

-

Economics: Macroeconomic Analysis97

-

Economics: Economics in a Global Context35

-

Financial Reporting and Analysis: Introduction46

-

Financial Reporting and Analysis: Income Statements, Balance Sheets, and Cash Flow Statements128

-

Financial Reporting and Analysis: Inventories, Long-Lived Assets, Income Taxes, and Non-Current Liabilities102

-

Financial Reporting and Analysis: Evaluating Financial Reporting Quality and Other Applications37

-

Corporate Finance92

-

Portfolio Management62

-

Equity Analysis and Valuation61

-

Fixed Income: Basic Concepts66

-

Fixed Income: Analysis and Valuation78

-

Derivatives76

-

Alternative Instruments30