Fixed Income #44 - The Arbitrage-Free Valuation Framework Flashcards

arbitrage-free valuation of a fixed-income securitiy

LOS 44.a

arbitrage-free valuation - method of valuing security such that no market participant can earn risk-free “arbitrage” profits using that security, i.e.:

- no initial cash outlay

- positive riskless profit in the future

- basic principle of “law of one price” in freely functioning markets

two types of arbitrage opportunities

LOS 44.a

arbitrage-free framework:

- upholds value additivity principle - value of whole differs from the sum of parts

- stripping: Vbond < strips ⇒ buy whole bond and sell its parts

- reconstitution: Vbond > strips ⇒ buy strips and sell the whole bond\

- does not allow for dominance - otherwise indentical securitiies having different market prices

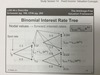

binomial interest rate model

LOS 44.c

binomial interest rate model - system for building interest rate models

- binomial tree with equal probability up/down interest rate paths

- lognormal random walk based on assumed volatility in interest rates (non-negative rates and higher volatility at higher rates

binomial interest rate tree

LOS 44.c

i0 → use spot rate s1

nodal values → use single period forward rate

i2,LU = i2,LLe2σ

i2,LU = i2,UL

i2,UU = i2,LLe4σ

FYI - know how to use the tree; won’t be building the tree on exam

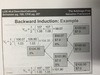

backward induction methodology

LOS 44.d

backward induction methodology - value a bond by moving backward from last period to time zero. Things to know:

- value at maturity is known

- value at any node is the average PV of the two possible values from next period

- discount rate used is the foreward rate of that node

backward induction example

LOS 44.d

calibrating a binomial interest rate tree to match a specific term structure

LOS 44.e

binomial interest rate tree must be calibrated to conform to 3 rules:

- arbitrage-free interest rate values

- adjacent forward rates (in the same time period) are 2σ apart

- middle forward rate (or mid-point for even number of rates) in a time period is ≈ implied (from benchmark spot rate curve) one-period forward rate for that period.

think “Ho-Lee” model