Chapter 8 Flashcards

(38 cards)

How is accounting profit calculated?

Profit (Loss) = Total Revenue - Explicit costs

What is Total Revenue?

The amount a firm receives from the sale of goods and services

What are explicit costs?

The amount a firm spends to produce and/or sell goods and services

How is Economic Profit calculated?

Economic Profit = total revenues - (explicit costs + implicit costs)

= accounting profit - implicit costs

What are explicit costs?

Tangible out of pocket expenses

What are implicit costs? Give an example.

The costs of resources already owned, for which no out-of-pocket payments are made.

eg. opportunity costs

How does accounting profit compare to economic profit?

Economic profit is always less than accounting profit

What is the production function?

The relationship between the inputs a firm uses and the output it creates

What are inputs?

A resource used in the production process to generate output

What are the three primary factors of production?

Labor, land and capital (LLC)

What are outputs (in relation to the production function)?

The product the firm creates

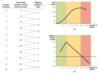

What is marginal product?

The change in output associated with one additional unit of input

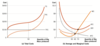

When does the point of diminishing marginal product occur?

When successive increases in inputs are associated with a slower rise in output.

- Firms should continue production as long as the revenue from output is more than the costs of input

Why does diminishing marginal product occur?

The firm is fixed in the short run and inputs are fully utilised

The gains from specialisation slowly decline

Describe the graph of marginal product

How do we calculate average total costs (ATC)?

= AVC + AFC = Total cost / Quantity (Q)

Why does the ATC rise?

Eventually, the increases in variable costs overwhelm the cost savings achieved by spreading fixed cost across more production

What are variable costs?

Costs that change with the rate of output

How do we calculate average variable costs?

TVC / Quantity (Q)

What are fixed costs (a.k.a overhead)?

Unavoidable costs that do not vary with output in the short run

How do we calculate average fixed costs?

TFC / Quantity (Q)

What happens to average fixed costs when output increases?

AFC declines

What is marginal cost?

The increase in cost that occurs from producing one additional unit of output

How is marginal costs calculated?

Change in total cost / Change in Quantity