Lecture 6 notes Flashcards

(71 cards)

What have we learnt in last couple weeks?

Valuing current assets Valuing non current assets tangible ( PPE inital, depreciation and disposals, revaluation, upward impairment)

What are we going to do today?

Valuing intangible non- current assets Equity section of SOFP Inventory, inital valuation, write-down valuation methods Sources of finance

What does Intangible mean?

You cannot touch or feel

Give examples of intangible assets?

Patents

Copyrights

Brands

Market share

Customer loyalty

What did we say earlier in previous lectures about intangible assets?

If you cannot be noted down in monetary terms, we cannot note it down, but now we will see when we can note it down and when we cannot.

For an intangible asset to be recognised as an intangible asset what 2 criteria must be derive?

1) Identifiable ( or separable)

2) Controlled by an entity

What does Identifiable mean as aa criteria for an asset to be intangible?

You should be able to sell it rent it, it should not be part of something else.

What does Controlled by an entity

The company must have full ownership of the asset, e,g, if you hire another company to do some research for you, and that company owns a patent, you will not be able to include that payment in your SOFP. You need to have control over it.

When are Intangible assets shown on the Statement of financial position?

An intangible asset is shown on the Statement of Financial Position only if the rights to some benefits are purchased.

When are intangible assets not shown on the statement of financial position?

Equally valuable assets may be created by internal expenditures, but they are rarely recognised as assets.

Give an example of a intangible asset being in the income statement and not being in the statement of financial position?

For example, suppose Winter Plc spends £5 million to internally develop and patent a new drug. Winter would charge £5 million to expense; no asset would be recognised. If Winter Plc had paid £5 million to another company for its patent, it would record the amount paid as an intangible asset

When will trade marks be recorded as intangible assets?

Only if they are purchased

Despite MacDonald’s and coca cola spend huge amounts of money on advertising and creating public awareness of their brands, does it show on the SOFP as an intangible asset?

It shows no intangible assets even though their brands are extremely valuable.

What is Good will?

It is an intangible asset, goodwill is the difference between what a company pays to buy an accquistion target, and what the accquired company is worth on paper.

Why do firms pay for good will?

You get brand value, employees etc, so you get the product as well as something else.

What is the Double entry for Good will?

Dr Net assets accquired (A-L)

Dr Goodwill account ( non-current asset)

Cr cash paid/ share issued.

What is an important thing to remember about Good will?

Goodwill is recognised as an asset in the acquirers’ accounts only after an acquisition e.g. Google acquires a small software company, google has paid extra goodwill, this is only recognised in Googles financial statement, not in the financial statements of the small software company.

( Subsequent measurement) After intial recognition of an intangible asset, how do you work out its net book value?

Cost or revalued amount - accumulated amortisation - accumulated impairment loss.

What is Accumulated amortisation?

Depreciation for an intangible asset.

How does the depreciable amount depend on whether the asset has a finite useful life or a infinite useful life?

If the asset is finite useful life, the depreciable amount should be allocated on a symmetric basis over the best estimate of useful economic life ( usually termed as amortization expense) If the intangible asset as a infinite useful life, it is only subject to impairment and not depreciated ( you cannot apply amortization

Company ABC has created a huge brand recognition through advertising. The cost of advertising is £100,000. The expected benefits is £5 million. What will be the value of the intangible asset – “brand value”

A) 100000

b) 5 million

c) 4,900,000

D) 0

D) 0 The brand recognition is internally generated not purchased, you don’t note down intangible assets like brand value when its internally generated.

Firm ABC acquired a permanent trademark from another firm. The accountant tells the CEO that they should amortise this intangible asset every year. Is the accountant correct? A) Yes B) No

B) This is no because to depreciate it must be a finite useful life asset. The word permanent implies infinite useful life, so you can’t amortise.

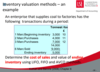

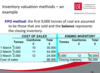

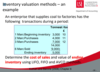

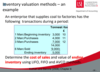

So Till now we were told the open opening inventory, what was the purchases and what was the closing inventory but how do we know the value of closing inventoy to come up with the cost of sales. What is the Cost of sales?

When goods are sold, their cost becomes an expense, ‘cost of sales’ Cost of sales = opening inventory + purchases - purchase returns - closing inventory

Lets consider you have 4 televisions 1) 100 2) 130 3) 150 4) 160 What is the Cost of goods sold it the first 2 are sold and what is the remaining inventory?

1) 100 + 130 = 230 cost of goods sold Closing inventory is 150 + 160 = £310.