Considerations when pricing Commercial Insurance Products

- Creation of homogeneous groups for ratemaking purposes not feasible 2. Some commercial risks are large enough to use their own experience (in whole or part) to price 3. Individual Risk Rating (IRR) -Price coverage provided more accurately than if rates were based in manual rates only -Balance risk sharing and risk bearing

Manual rate modification mechanisms

-Experience rating -Schedule rating

Rating techniques for large commercial insureds

-Large deductible plans -Loss-rated composite rating -Retrospective rating plans

Actual and expected experience may be compared in following ways for experience period

-Actual paid loss & ALAE with expected paid loss & ALAE -Actual reported loss & ALAE with expected reported loss & ALAE -Projected ultimate loss & ALAE with expected ultimate loss & ALAE -Projected ultimate loss & ALAE adjusted to current exposure and dollar levels with expected loss & ALAE based upon current exposure and dollar levels

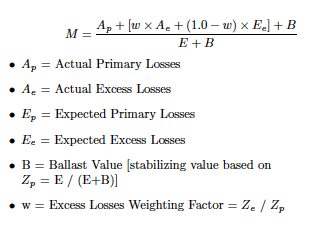

Formula for computing GL ERP credit/debit

CD=( (AER - EER) / EER) x Z

Calculation Subject B/L L&ALAE Costs

- Company Subject B/L L&ALAE Costs 2. Calculate Reported Losses and ALAE Limited by Basic Limits and MSL 3. Add Expected Unreported Losses and ALAE Limited by Basic Limits and MSL 4. AER = (b. + c.) / (1)

NCCI Formula with substitutions for primary and excess credibility

Schedule Rating

- Does not directly reflect claim experience 2. Recognizes characteristics expected to have material effect on experience that are not actually reflected in experience -Changes in exposure -Changes in risk control programs -Used when risk too small to qualify for experience or composite rating 3. May be used on objective criteria or subjective underwriting judgment

Composite Rating

- Large, complex risks use a single, composite, exposure base instead of several for many different coverages 2. Composite rate determined at the beginning of the policy period using historical exposures -May be determined using manual rates with experience and/or schedule mods -Depending on size, may be based solely on insured’s own experience (aka Loss Rated) 3. After expiration, audited to determine composite exposures.

Pricing Considerations of Large Deductible Policies

-Claims handling –insurer may handle all claims, even if below deductible -Application of Deductible –may apply only to losses or losses & ALAE -Deductible Processing –insurer may pay cost of entire claim and then seek reimbursement from company for amounts below deductible

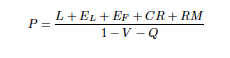

Formula to calculate premium of Large Deductible Policy

- CR = Credit Risk

- RM = Risk Margin

Basic Retrospective Rating Formula

Retro Rating = (Basic Premium + Covered Losses) x Tax Multiplier

Basic Premium

Intended to provide for

- Insurer’s target underwriting profit and expenses excluding expenses provided for by LCF and tax multiplier

- Net charge for limiting the retro premium between minimum and maximum

- Cost of limiting each occurrence, if applicable

Standard Premium

-Insurance premium for risk before consideration of retro plan and any premium discount -Determined on basis of exposure, insurer’s rates, experience mod, and any premium charges excluding premium discount

Insurance Charge and Insurance Savings

-Insurance Charge is an estimate of cost to insurer associated with retro max -Insurance savings is an estimate of savings to insurer for requiring a min premium